Sketchy Business

Posted by John Vrooman on Thursday, January 30, 2020 in Major League Soccer, Sports Econ Blog.

Interview with Fortune Magazine 1/30/20 / Interview with graphics.

I’m a reporter for Fortune currently working on a story for our upcoming magazine issue that focuses on Major League Soccer’s rapid economic and geographical expansion in recent years. In particular, I’m focusing on the extent to which the league has grown its footprint, how team values have reportedly climbed and how an influx of notable business people and high-worth individuals have bought into the league’s teams recently—while also examining the challenges and limitations of the league’s economic model and whether some of this expansion into new markets could be a case of too much, too soon for the league.

I noticed you’ve spoken on the topic of MLS’s economics with other publications, and as such would greatly appreciate some of your time and insight for my story. I’m speaking to folks at MLS and owners at some of the clubs, but would value the thoughts of an impartial outside observer with a firm grasp on sports economics and the business model of this league, in particular.

Fortune Interview with John Vrooman 1/30/20

- What, in your estimation, are the biggest reasons that the league’s franchise values reportedly continue to increase to record levels? Similarly, what is driving the increased entry fees being paid by new expansion teams?

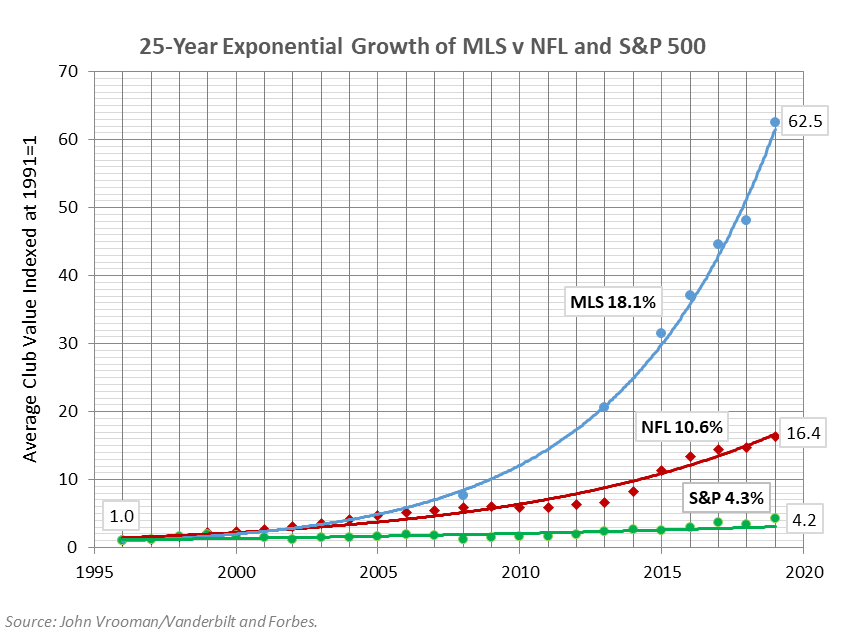

The MLS expansion fees are being driven largely by a market power of a sports league monopoly cartel. Over the quarter century of its existence the financial value (expected price) of the average MLS franchise has increased at an exponential rate of 18.1 percent, about 1.7 times as fast as the NFL juggernaut and more than four times faster than the S&P 500 (the best competitive market rate available).

A somewhat risky MLS founders’ investment in 1996 would currently be valued at 4 times the same investment in the closed NFL, which in turn would be valued at 4 times the same investment in the open market S&P 500. These above competitive market yields serve as prima facie evidence (proof) of the monopoly power of these closed Leagues as seemingly invincible cartels.

Theoretically, a competitive expansion fee would be set where the expected value of net risk-adjusted cash flow from the franchise was equal to the extra expansion costs borne by the existing club owners (such as dilution of shared media rights and gate revenues and increased competition for talent.)

The monopoly power of a sports league cartel (limited expansion slots with several bidders) usually inflates the auction price by about 25%-30%. For example in the most recent Charlotte expansion case, NFL Panthers owner David Tepper is paying a whopping $325 million fee, which carries an additional premium of $50 million to $75 million on top of an already inflated auction price estimate of $250 million, just to blow away the potential competition — NFL ownership money talked and MLS listened.

- Do you think the league is expanding too quickly? Why or why not? How big could you see the league growing, as far as number of teams?

This is a tricky question, because there are two directly opposing league expansion optima. The first is based on the league size that would maximize internal total league profit or value, whereas the second optimum size would max out the total social welfare of all fans, players and owners combined.

The major economic problem has always been that the latter social welfare optimum is sacrificed at the expense of the former, because of the artificial monopoly power of sports league cartels. The owners always max out the internal optimum (and pyramid scheme expansion fees) at the expense of the external social optimum (and fan and player welfare). Monopoly clubs and leagues charge half as many fans more than twice as much, and pay its players half as much a competitive league.

The internal optimum MLS league size maximizes artificial expansion fees that can be charged to a select few of several competing franchise hopefuls in a monopoly MLS franchise auction that currently pits 10-12 markets against each other for 2-4 artificially limited franchises. It is easy to show that the winners of a monopoly franchise auction systematically overpay a franchise fee that exceeds the present value of the club’s cash flow by 25% to 30%. This is aptly named the “winner’s curse.”

The current MLS franchise fee is arbitrarily determined and has absolutely nothing to do with the real cost to the league of adding new members. As a result the current expansion fees will exceed the ability of the new clubs to pay the fee from future cash flow. The cash-flow numbers just don’t add up to the inflated cartel expansion fees, and the winning franchises will probably seek a heavy public subsidy, or live off future fees in accordance with the MLS pyramid expansion scheme.

The socially optimizing league would be comprised of teams from all markets that could generate a positive profit and the expansion fee would only cover the true cost of league expansion to the existing MLS members. So in the case of the MLS the internally optimal size could be the current 30 MLS clubs, compared to the socially optimizing size of at least 36 to 40 clubs.

This is especially true for an isolated MLS league that relies on mediocre talent drawn from an extremely limited or nonexistent player development pyramid, without the promotion and relegation of clubs among multi-tiered leagues as is found throughout the rest of the unified football/soccer universe.

The most obvious suggestion would be to have 40 clubs or more (even 60) subdivided into two (or 3) tiers naturally separated in quality by promotion and relegation between seasons. There are no inflated expansion fees in European football where the clubs reach the top flight through the quality of their play.

Instead of artificially inflating the expansion membership fees from an artificially scarce number of slots, the MLS should probably expand to at least 36 to 40 teams and merge with the NASL and USL (which is already happening) to form a multi-tiered North American soccer pyramid.

MLS teams will begin to clear profits when the League quits expanding like a financial pyramid scheme and vertically integrates with other minor Leagues to form a traditional European soccer player-development pyramid with conventional promotion and relegation of teams from season to season.

This is probably the only way to merge the internally and externally optimal league sizes, and Improving the quality of play on the pitch on par with the rest of the soccer universe would begin to internalize the current externalization of growth through expansion extortion.

- Unlike other North American pro sports leagues, MLS deploys a more centralized “investor/operator” model that features greater revenue sharing and coordination between teams at the league-wide office level (at the expense of autonomy at the individual club level). What would you characterize as the pros and cons of this model, and do you think it bodes well (or not?) for the league’s economic growth prospects in the future?

In terms of social welfare, the ideal model for a sports league is for the franchises to be separately owned with a minimum general partnership share. The single entity common ownership scheme may be a temporary and risk reducing way for an infant industry league to survive, but as the league matures and develops the original multiple club owners like Lamar Hunt and AEG in the adolescent MLS to divest ownership in all but one of their clubs. The steady state is for all clubs to become financially independent and separately owned.

As a single-ownership league matures it should evolve into several and separate owners. The timing problem for is for the single-entity league have enough solidarity (NFL owners called this “league think’ during the AFL rival league war 1960-67) to survive the financial polarization and imbalance of talent that profit maximizing independent clubs will probably create in the beginning.

At the other extreme, a successful “several and separate ownership” league will probably by necessity or be restricted by revenue sharing, equity ownership requirements and debt rules with labor markets limited by salary caps, which at the limit mimic the single-entity format. The joint nature of games/matches constantly raises legal questions about whether the league is the firm or a cartel of club-firms. The correct answer is probably both, and the degree of cartelization is directly related to the amount of revenue and costs (profits) that are shared.

As they mature, single entity (MLS now) and multiple ownership leagues (NFL in 1960) will both coevolve and morph into similar structures. Clubs in a single entity league will ultimately become individually owned (MLS future), and clubs in a multiple ownership league will share revenues and regulate player costs and owner equity and debt to the extent that the league will become a pure syndicate at the limit (NFL now). (see attached zeta distribution comparison)

- Some high-profile, successful figures in the world of business and finance (Meg Whitman, Joe Mansueto, Ron Burkle, David Tepper) have recently bought into or helped found MLS franchises. Beyond personal, intrinsic or image-related factors, what would you say is the financial/economic/business case for owning and operating an MLS franchise? Do you think it’s a prudent long-term investment?

Beyond intrinsic sporting value and the synergistic risk diversification advantages of multiple team ownership, it is important to realize that after all is said and done about the “beautiful game,” a closed sports league is an unregulated monopoly cartel with a license to exploit fans, players and tax-payers.

If the MLS charges an arbitrary expansion fee equal to the value of the average existing club (Charlotte was hit with a $325 million fee), then the present value of the cash flow of an expansion franchise is exhausted before the club even plays a match. The MLS investment pyramid may therefore seem like extremely sketchy business at best, but when seen as a risk-free cash-cow easy-money monopoly machine, sports-franchise ownership is a natural-born sure thing.

- Most MLS franchises struggle to turn a profit. What are the biggest obstacles standing in the path to profitability for these teams, and what can the league do to help improve the bottom line?

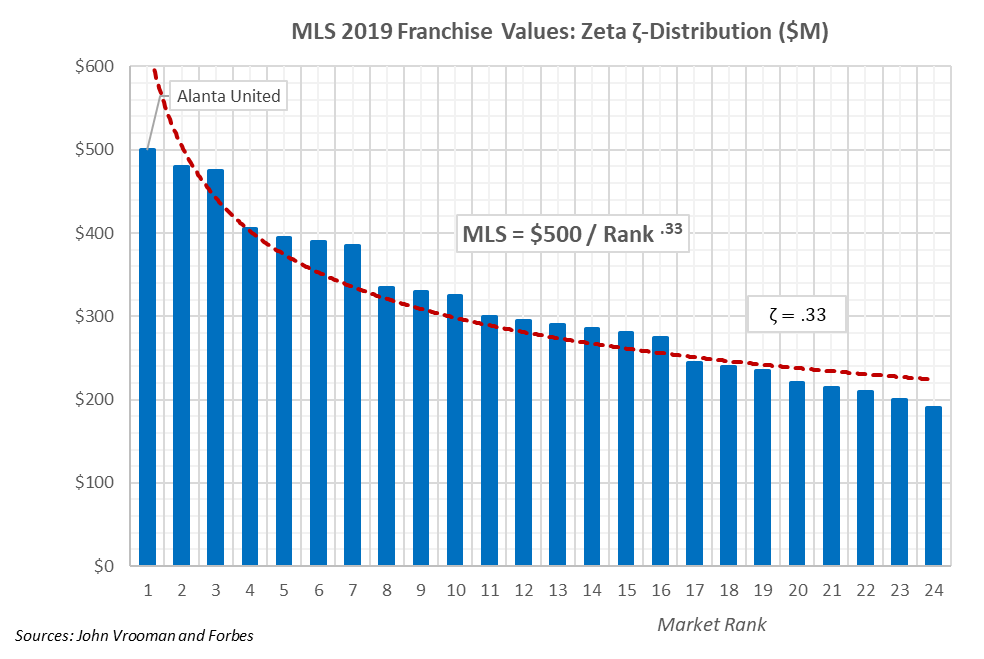

Forbes estimates the value of an average MLS club in 2019 was about $313 million and MLS total losses of $105 million on league revenues of 816 million. (See Value charts). The NFL obviously dwarfs the total MLS numbers with an average team value of $2.9 billion and total operating profit of $3.3 billion on revenues of almost $15 billion, but the revenue distribution among markets is notably about the same.

See attached zeta distribution graph comparison, where MLS zeta = .33 compared to NFL zeta = .25. If zeta = 0 then all markets are equal and as zeta increases, the value distribution of clubs becomes more unequal from top to bottom.

This is the result of the converging egalitarian ownership structures of the two fully diversified leagues, as discussed earlier. Although both leagues are at opposite stages of development, they both realize that any franchise is really only as strong as its weakest opponent.

Revenue sharing in a sports league creates a perfectly diversified cash flow because of the perfectly negative correlation of outcomes in a sports league. A revenue sharing league is a perfect team-specific risk-reduction portfolio.

The most pressing problem for MLS is clearly the need for increased in equally shared media revenues, which derive directly from healthier national ratings from an improved product on the pitch. Inferior quality of MLS play is one of the unfortunate side effects of its rapid pyramid expansion.

The ultimate remedy is to expand toward 40 clubs and split the league into 20-club MLS1 and MLS2 tiers, where the premier league MLS1 is populated by promotion and relegation to and from a developmental MLS2. This is the only way for the US to play the beautiful game on par with the rest of the football world.

- The league’s next TV deal will be renegotiated in advance of the 2023 season. With MLS games still behind in ratings compared to Liga MX and even weekend morning Premier League games, do you think the league will be able to command a significantly improved package for its broadcast TV rights?

MLS has been engaged in a well-engineered progressive pyramid expansion extortion scheme over the last 25 years. The evolution of soccer popularity in the US is similar to the evolution theory of punctuated equilibrium, where gradual evolution (expansion) is punctuated by sudden jumps or leaps.

The economic key to MLS expansion is the demographics of the two US coasts for match day attendance but the key to MLS long-term survival are national media rights which also require a multiple presence in mega media markets.

Accordingly, MLS has strategically handled location and its overall expansion footprint has been set. It time for the league to fill in the missing markets (MLS1+MLS2 = 40) and restructure itself into a healthy player development pyramid, rather than a self-consuming expansion extortion pyramid.

The World Cup and Olympic games are external mega-events that cause sudden demand-side pressure for change which punctuate these longer period of slow growth. The gradual continental drift forces are of course the changing demographics of North America and increased competition among cable sports channels desperately seeking live inventory in the face of the new media revolution (streaming).

The driving force is not necessarily coming from ESPN itself, but more from the new competition among NBC, FOX seeking to emulate ESPN on ABC. This competition is also a derivative of NBC’s deal with EPL and FOX’s outbidding NBC for current MLS rights and future World Cup rights. This increases North American exposure to soccer and artificially inflates the media rights fees necessary for league survival. Unfortunately MLS games only have half of the viewers in the US as either EPL or Liga MX.

The major media competition in the US seems to be coming from the popularity of Liga MX and EPL in North America. Although current MLS rights fees quadrupled with FOX and ESPN/Univision, EPL rights soften the competition among the 3 bidders. While the popularity of soccer on TV is growing in the US, Liga MX and the EPL are benefitting the most, while MLS growth has become stagnant, and declining in 2019 to about 268,000.

Improving the quality of play on the pitch and expansion of national media are the key survival goals for the post-adolescent MLS. The immediate match of most importance now is the bi-lateral bargaining game between the monopoly league and the monopsony sports networks before 2022.

Average Viewership on US TV

| Year | Liga MX | MLS | EPL |

| 2016 | 585,049 | 273,321 | 394,452 |

| 2017 | 550,862 | 285,285 | 364,531 |

| 2018 | 459,287 | 290,278 | 428,503 |

Here are series of MLS interviews that may answer most your questions about the economic performance of the League.

|

Posted by John Vrooman on Monday, December 16, 2019 in Major League Soccer, Sports Econ Blog.. Interview with Charlotte Business Journal / Atlanta Business Chronicle / Expansion Derby.. MLS is going to name Charlotte as its next expansion city with an announcement Tuesday. Carolina Panthers owner is expected to pay $300 million to $325 million for a team that will share the NFL stadium (with … my.vanderbilt.edu |

|

Posted by John Vrooman on Tuesday, July 9, 2019 in Major League Soccer, Sports Econ Blog.. Interview with Charlotte Business Journal. MLS Expansion Game: Past Present and Future. Could you share a thought or two on what you think Charlotte’s chances are for landing a team and what you think the odds are for it working here? my.vanderbilt.edu |

https://my.vanderbilt.edu/vrooman/2018/03/devils-in-the-details/

|

Devil in the Details. … Posted by John Vrooman on Monday, March 5, 2018 in Major League Soccer.. Interview with Austin Biz Journal.. MLS Stadium Deals. Does the $400 million ‘community benefit’ impact over the club’s first 25 years seem plausible given other MLS stadium impacts? my.vanderbilt.edu |

|

Posted by John Vrooman on Monday, September 11, 2017 in Major League Soccer.. Interview with ESPN FC.. What’s the optimal size of the league for the number of teams? In terms of supply and demand and market support, should it keep expanding? my.vanderbilt.edu |

https://my.vanderbilt.edu/vrooman/2014/08/continental-drift/

|

Posted by John Vrooman on Friday, August 8, 2014 in Major League Soccer.. Interview with CNBC. How does a league decide how many teams it should have? Is the MLS being smart with a jump from 19 teams now, to a planned 24 by 2020? my.vanderbilt.edu |

Enjoy.

jv

©2024 Vanderbilt University · John Vrooman

Site Development: University Web Communications